1. Intro

GEA (ticker : GEA) manufactures highway toll equipment. In my area (Escota highway network, owned by Vinci Group), almost every automatic toll I see is badged GEA.The company has already been covered by several bloggers, which will spare me time :

- Actions ordinaires entreprises extraordinaires : Here and here (in French)

- Trying to be like warren : Here (in French and partially in English)

- The Red Corner : here (in English) , a very interesting and impressive analysis. I've added the blog to my blogroll.

To sum it up :

- GEA currently (for a quote of 65 €) trades at EV/EBIT ~ 2x, PER ~ 9 (2011 results)

- 2011 operating margin 22% (before taxes), 2011 ROE 22 %

- 0 debt, 40 m€ cash for a market cap of 78 m€, no goodwill

- order backlog covers more than 1 year of activity,

- low maintenance CAPEX requirements

The company supplies 85 % of French motorways and has sold its toll systems in 33 countries worldwide.

All this sounds too good to be true and of course the question is : why is it so cheap ?

As pointed out by the Red Corner blog, there's a dramatic improvement of the business after 2007 (both sales and margins) : why ?

Another chart illustrating this (net result) :

The underlying issue of course is what will the future look like ? As pre-2007 (the current valuation is justified) or more like the recent years (then the current valuation is a bargain) ?

Second point : GEA is cheap because of its large cash position and absence of debt. Where will this cash go ?

2. Drivers behind the business improvement

I've read the annual reports but the management does not supply a clear explanation or I've missed it.The Red Corner blog article attributes this to international sales and a greater mix of services (maintenance,...) with a higher margin.

Here is what I found on my side.

What has driven the sales growth ?

Many highways went private in 2005 and embarked on an automatic toll collection program in the late 2000's. Here is an article giving the number of highway employees working in toll collection. The gain in productivity for highway companies is immediate and the return on this investment is quick.

Electronic toll collection in French highways mainly relies on a DSRC (dedicated short range communication system) and a transponder or tag that is placed in the vehicle : Liber-t system in France (all highway operators use the same standard).

Other technologies have been developped (for instance satellite-based systems).

See for instance this neat presentation by Kapsch TrafficCom, a competitor of GEA (based in Austria)

For example according to this release, ~50 % of transactions on the APPR highway network are now made with this system and automatic transactions represent ~90 % of the total transactions. Almost all toll plazzas are now completely or partially automated.

So the market is probably saturated here.

In 2010 the highway companies signed with the Government a "green" investment program of 1 bn€ in exchange for a extended public concession time (so called "paquet vert" ="Green package") : article. One of these investments is the immediate deployment of a 30 km/h drive-though toll in dedicated lanes; cars and trucks won't have to stop and restart, which reduces CO2 emissions.

GEA will benefit from this (see for instance GEA presentation here).

In 2013 all trucks will have to pay taxes on the national roads and smaller departmental roads : see link here. Apparently the system involves "free-flow" tolling using overhead gantries and an on board unit (OBU). However I do not see GEA appear in the list of the Ecomouv company partners).

Free-flow tolling is the logical next step for highways and GEA should benefit from that.

In this article, there is an interview of Grigori Zass, the son of the company founder Serge Zass (in French).

A few items roughly translated :

- CAPEX requirements are low (~300 k€) but about 5 % of the salaries can be considered as R&D investments (1-2 m€/year)

- we were late in developping a "free-flow" system ; it was a mistake because it's the future and competitors are ready

- the French market remains central for GEA : few new highways are expected, but toll systems have to be maintained, upgraded every 3-5 years and replaced every 10 years "We live from this renewal/evolution market"

- export markets are difficult, especially China (local suppliers tried to copy their products). The product is 1st launched/tested on the French market, then made available for export

- same trend towards automatization on international markets

- in France the market has concentrated (more on that later)

Margins

GEA does not provide a breakdown of margins by business segment but its competitor Kapsch does :

Double-digit operating margins for services, extensions,... (recurring part of the business), much more fluctuating for the new projects (one-time effects). But of course you can't have the first business without the second.

I think this explains GEA 2005 loss. The 2005 annual report (loosely translated) says "this year an unusually high number of new pluri-annual contracts have been started, which significantly impacted the (net) result. The (positive) effects will be felt in 3-5 years".

I think that GEA currently benefits from long-term contracts signed a few years ago when French highways embarked on a large automatization program. I think this will slow down but the overall trend is positive.

Competitors and comparables

Main local competitor is the transport branch of group "Communication et Systemes" : link.

The Sanef group (itself a subsidiary of Spanish Group Abertis) has recently made an offer to buy the transport branch of CS, for a yet undisclosed amount.

Another French competitor is Thales (apparently it's a little more complicated because Thales has collaborated with GEA in the past to produce tags). Toll collection is just one of the numerous activities of Thales.

Another one is Multitoll apparently a former subsidiary of Ascom group (Swiss), now independent.

Other competitors I could identify are Kapsch (already mentionned), Q-Free, from Norway, and SICE from Spain.

Kapsch and Q-Free are listed companies, SICE and Multitoll apparently not.

See below the operating margins of competitor Kapsch (the 2011 surge in sales is linked to a major contract in Poland)

{kind=link}

The 2004-2011 average operating margin is around 10 % for GEA, 13 % for Kapsch, 5 % for Q-Free

According to the 2011 CS annual report, operational result 1.4 /sales 31 m€ = 4.5 % for the transport branch.

Multitoll is privately owned but you can find some info here. Operating margins are around 4.4 %.

So I don't think that the current margins of GEA (>20 %) are sustainable in the future.

3. What will happen to the cash ?

GEA has 40 m€ in cash and 0 debt. What will happen to this cash ? Will it go back to ordinary shareholders ?GEA is a small familial company, founded in 1970. The founder has 33 % of outstanding shares and more than 50 % of shareholder votes.

In the annual reports I have seen no trace of golden parachutes, free shares, stock-options, special retirement packages and related stuff. Management salaries seem very reasonnable.

The company pays a dividend (current yield 3.4 %), but there is no notable share buy-back program.

In the above mentioned article, Mr Zass states that GEA went to the stockmarket in 1994 to find capital to fund its exportation effort and that GEA independence is fundamental : "we wanted neither to sell our company to a larger group or to be indebted to banks".

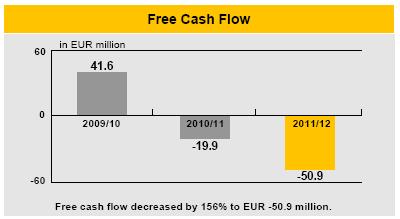

Given this state of mind, I hardly imagine GEA giving this cash back to shareholders as a special dividend or a major share buyback. I think that GEA would need this cash in case of a large export contract, because cash flow can be very negative during some phases of the contract ; see for instance the free cash flow of Kapsch.

4. Conclusion

Ce que l'on conçoit bien s'énonce clairement. Et les mots pour le dire arrivent aisément.In my case, just the opposite. I spent a long time writing and deleting this paragraph, which shows that I have a hard time reaching a clear conclusion.

All the bloggers mentionned at the beginning are very positive about GEA.

I'm not sure at all about extrapolating GEA recent results in the future (but 2012HY results are good ; some slowdown in sales but strong margins).

On the other hand, GEA valuation is very low compared to its competitors Kapsch and Q-Free. 2011 EV/EBIT ratios are around 16 for these two.

In 2008 it was possible to buy GEA at 10 €/share, an incredible deal offered by Mr Market (with the benefit of 100 % hindsight). Is it too late now ?

Insider trading : some buying by the family mid-2010 at around 40 €, nothing since.

A very simple DCF valuation (perpetuity) :

So the current price (around 65 €) is consistent with these assumptions :

- 0 growth

- 10 % EBIT margin (reversion to the mean)

- around 13 % required return / discount rate.

So am I willing to "buy" this company with reasonnably conservative assumptions about its future, and a return of ~13 % ? Yes. Do I have a large margin of safety ? Not sure.

Disclosure : long GEA.

Salut, et merci pour cette analyse perspicace.

RépondreSupprimerGreat analysis Caque!

RépondreSupprimerGEA is a buy and hold share in my opinion. Patience will be our ally. I agree with you, we won't be seing a repurchase program. I would think that they will keep increasing the dividend slowly and surely as they have done for the last couple of years.

Great research of articles which are really instructive especially the one from the journal des entreprises.

The Kapsch elements are really useful for the toll business and enable us to fully understand the cash generation process.

In the annual report of 2009,2010 there was a dispute with a software company but there wasn't any trace of it in the 2011 annual report. Do you have an idea of what happened?

I will try and give them a ring and see if they can give us more insight.

Keep up the great work!

Cheers

Jeremy

Bonjour Jeremy

SupprimerNon je n'avais pas fait attention à ce litige, je vais regarder.

Cordialement

Good afternoon,

RépondreSupprimerGood job. Thanks.

I’m impressed by Kapsch revenue, an austrian company operating in the same business than GEA.

Questions for you.

1/ Do you know Kapsch and Q-Free market value, share price and dividend? (+ Q-Free revenue)

2/ Do you know Kaspsch international revenue (I think that part of GEA international revenue is related to their French customers)

It appears clearly that GEA is too small. Something must happen, but what?

Regards

CPaulus

Bonjour CPaulus, je crois qu'on peut basculer au Français.

SupprimerOn peut trouver des infos sur l'action Kapsch ici

http://www.kapsch.net/en/ktc/investor_relations/share/Pages/default.aspx

Pour un cours de 50 €, la CB est de 650 m€.

Dividende = 0 cette année, 1 € l'année dernière.

En 2011/2012 l'Autriche ne réprésente que 6 % du CA du Kapsch, tout le reste est à l'export. Impressionnant.

Kapsch est notamment présente aux US

http://www.tollroadsnews.com/node/5394

Sur Q-Free je compléterai ultérieurement.

Donc oui, GEA est solide sur le marché français mais je pense à l'export la concurrence doit être rude.

Cordialement

Good objective analysis that puts on the table questions about the future growth.

RépondreSupprimerHi.Just looked at GEA.At first glance,it had looked like a company with stable revenues that is accumulating cash.Things that puzzled me in the balance sheet,though,for the year ending September 2012.Accounts receivable and inventory both rose sharply,whereas liquid investments remained stable.This is not what I would have expected from a company that facilitates toll payments,which should not be experiencing delays in obtaining payment from its customers,since its customers should have stable,guaranteed revenues from its customers.Liabilities in the form of deferred revenues and accounts payable rose too - what would be the need for that from a company with plenty of cash/liquid assets ?

RépondreSupprimerHi.

RépondreSupprimerAccounts receivables and inventory increased from 2011/2012 but decreased from 2012/2013. The 2013 annual report says in the footnotes (n°8) that (my translation) export contracts are charged to the customer when the work is accepted by the customer and after the customer has given its green light for payment. For the other contracts, the report says that the invoice is sent according to the progress and negotiated terms. So maybe this can explain this temporary increase.

Regarding the accounts payable they pay in 30/60 days, nothing unusual I guess ?

Hi,

RépondreSupprimerI´m interested in analysing the company but i can´t find the 2013 annual report. Do you know where can i get that document? i look into GEA website but the latest one is from 2011/2012. Do you have acess to any financial release from the current year to?

One of my concerns about the company is related with the decrease in the earnings for 2014, any specific reason? I can´t find anything related to this expectations.

Thanks for your attention.

Hi

SupprimerSeems that only the French version has been published. Apparently GEA hasn't bothered to translate it in English yet,

The 2013 annual report is here : http://www.gea.fr/Francais/pdf/GEA-rapport-annuel-13web.pdf

The 2014 HY report is here: http://www.gea.fr/Francais/pdf/GEA_RF%20semestriel%202014.pdf

Regarding the 2014 decrease, see my blog entry here:

http://valueinvestingfrance.blogspot.fr/2014/05/gea-hy14-results-q-free-comparison.html

The main reason is that the French market seems saturated and export is difficult.

Regards